The $12 Billion Power Race: How MENA's Energy Giants Are Betting Big on the AI Data Center Boom

MENA’s Next Power Play: Why Data Centers Are Becoming the Region’s Most Important Energy Opportunity

The MENA region is entering a new phase of growth, and this one is moving fast.

For years, the energy story in the region was defined by oil, gas, and large-scale infrastructure. Now a new demand center is rising just as aggressively: data centers. That shift matters because it is happening at the exact same time governments are pushing hard on decarbonization, economic diversification, and digital sovereignty.

What this really means is simple. In MENA, energy transition and digital transformation are no longer separate stories. They are becoming the same story.

And the companies that understand this early will be in a strong position to shape the next decade.

A Region in Dual Transformation

Across the Gulf, national strategies are changing the economic map.

Saudi Vision 2030 is accelerating diversification at scale. The UAE’s Net Zero 2050 pathway is pushing the country toward a lower-carbon energy mix. At the same time, AI adoption, cloud expansion, and data localization requirements are driving a surge in data center construction across the region.

This is not a niche trend. It is a structural change in electricity demand.

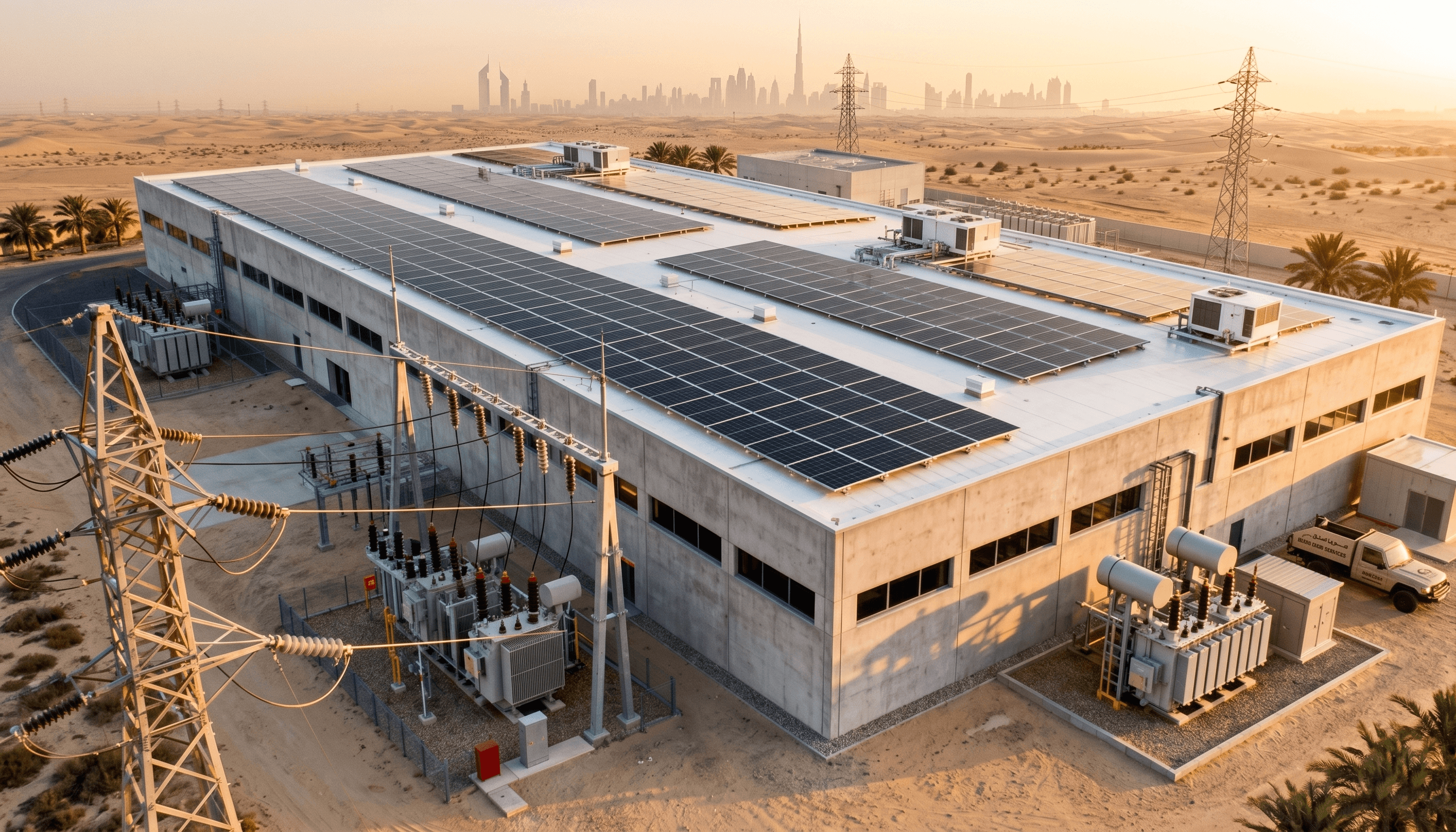

Existing regional data center capacity stood at roughly 1 to 1.6 GW in 2025. By 2027 to 2028, upcoming projects are expected to add another 4.5 to 6 GW or more. That buildout represents an estimated 8 to 12 billion dollars in investment.

Those numbers are large on their own. They become even more significant when you consider the type of power data centers need: constant, high-quality, interruption-free electricity, every hour of every day.

Why Saudi Arabia and the UAE Are Leading

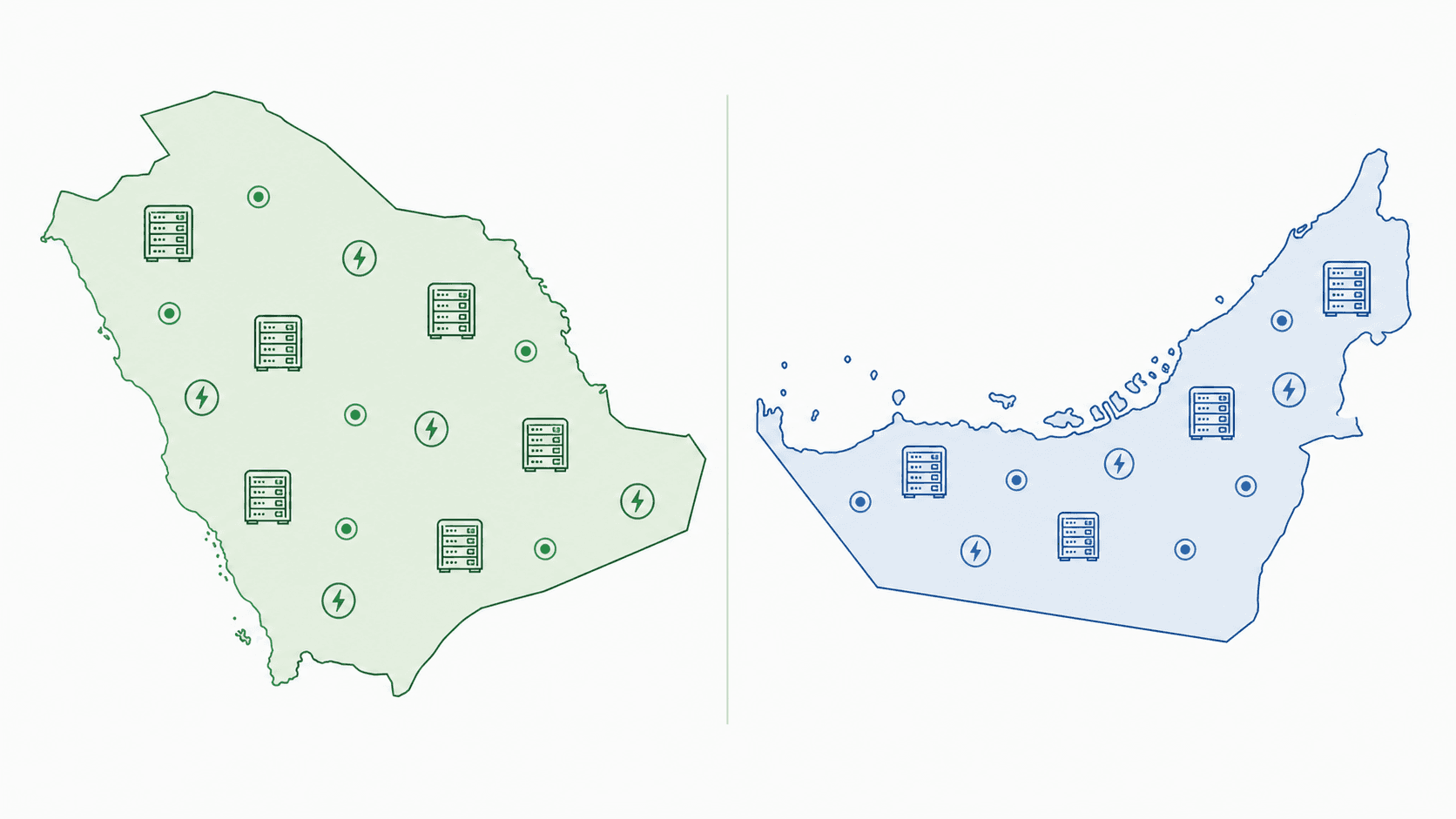

Saudi Arabia is positioned to dominate the next wave of regional data center growth.

The Kingdom accounts for more than 45% of upcoming power capacity tied to this buildout. That momentum is being driven by sovereign AI ambitions, cloud expansion, and data localization policies that keep more compute infrastructure inside the country.

The UAE is close behind, and its trajectory is equally important. Data center electricity consumption there is projected to rise from around 3 TWh in 2025 to more than 6 TWh by 2030. That would put data centers at roughly 2% to 3% or more of national electricity demand, with AI workloads likely pushing the share even higher.

Here’s the thing: this is not just about more servers. It is about a new category of strategic national infrastructure.

Data centers now sit at the intersection of:

Economic diversification.

AI leadership.

Digital sovereignty.

Industrial policy.

Grid planning.

Energy investment.

That combination makes them one of the most important demand drivers in the region.

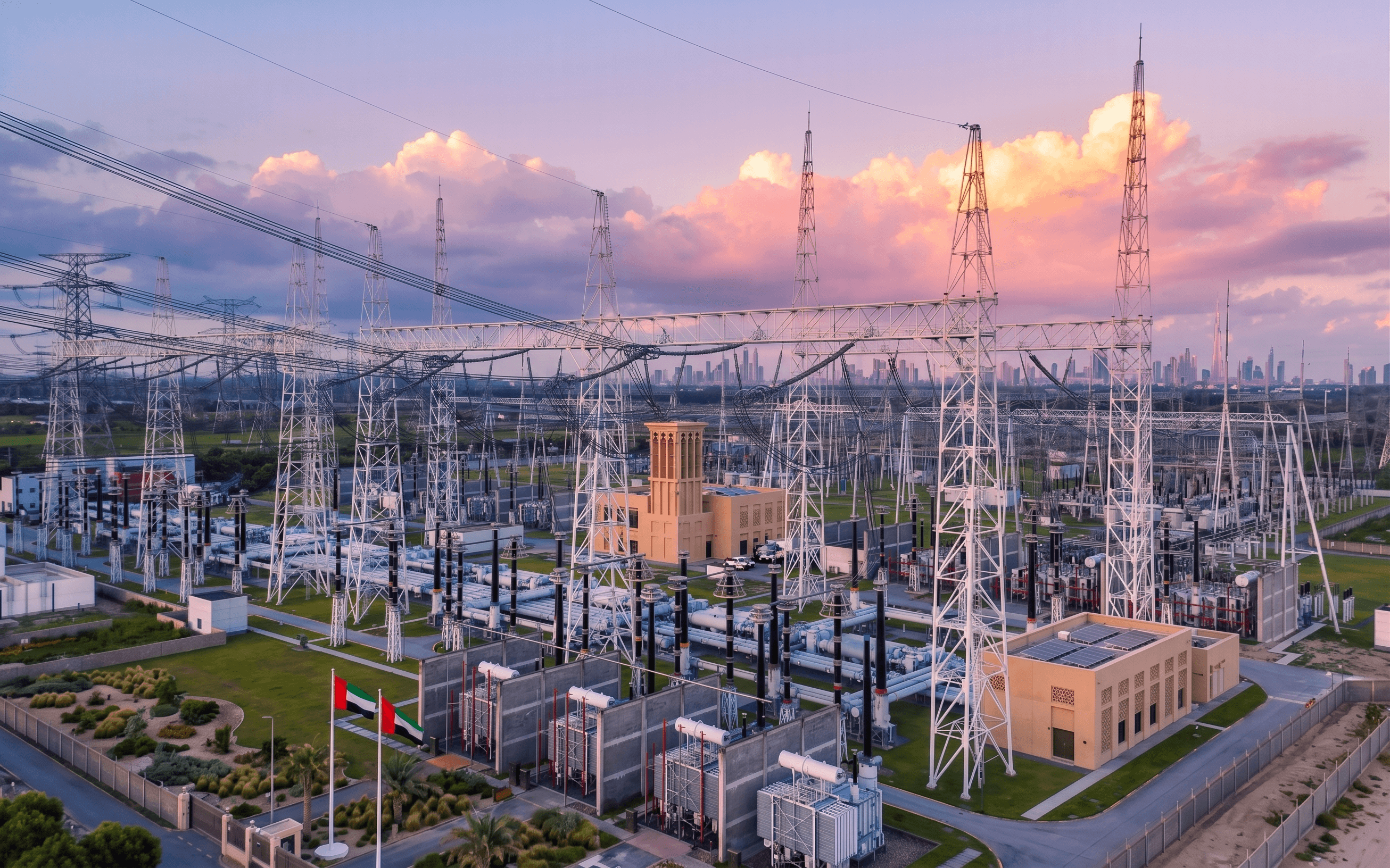

The Real Constraint Is Not Land or Capital, It Is Power Quality

It is easy to talk about gigawatts. The harder question is what kind of electricity can actually support hyperscale and AI workloads.

Data centers are extremely sensitive assets. They require uptime of 99.999%, which leaves almost no room for instability. Even short interruptions can create major operational and financial risk.

That is why the region’s energy leaders are in such a strong position.

Companies like Saudi Aramco, ADNOC, ACWA Power, Masdar, DEWA, EWEC, and QatarEnergy are no longer operating with a narrow hydrocarbon mindset. They are repositioning around an energy system that must do three things at once:

Deliver scale.

Cut emissions.

Guarantee reliability.

That is a difficult combination. But MENA has structural advantages that few regions can match.

MENA’s Competitive Energy Stack

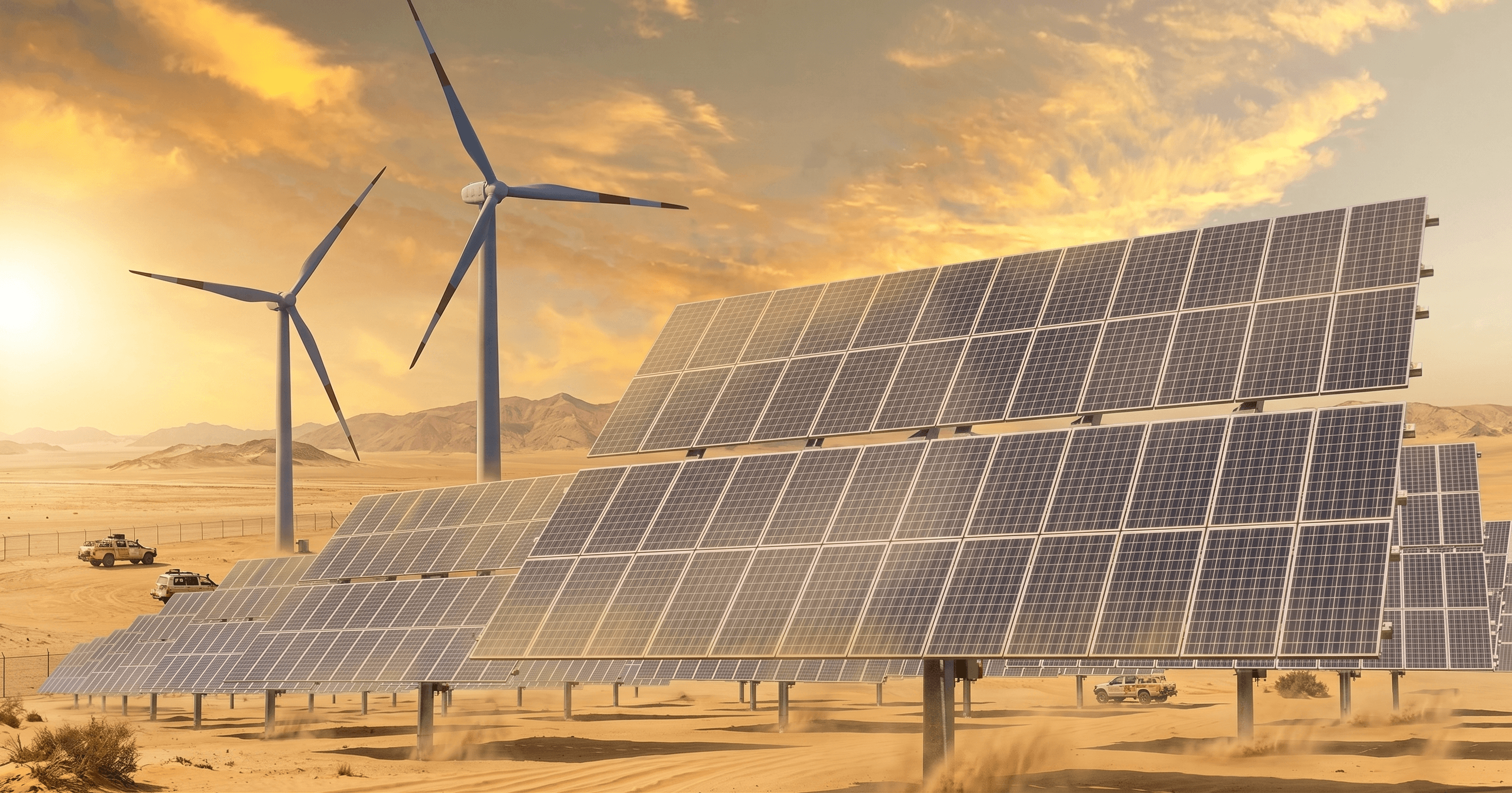

The region’s opportunity comes from its ability to combine multiple energy sources into one compelling offer.

Low-cost solar

MENA has some of the best solar economics in the world, with record tariffs near 0.01 dollars per kWh. That gives energy developers a strong foundation for lower-cost, lower-carbon electricity.

Gas for flexibility and backup

Natural gas remains critical because it provides dispatchable power when solar output falls or demand spikes. For data centers, that flexibility is not optional. It is part of the reliability equation.

Nuclear for a stable baseload

The UAE’s Barakah nuclear plant, with full capacity at 5.6 GW, adds another major advantage. Nuclear offers steady, low-carbon baseload generation that can support large, uninterrupted demand profiles.

Grid modernization

Modern transmission, digital controls, and smarter load balancing will play a central role in matching variable renewable supply with mission-critical demand. Grid intelligence is becoming just as important as generation capacity.

Put together, this gives MENA something highly valuable: the ability to offer “always-on” power that is cleaner than legacy systems, but more reliable than a renewables-only model can currently provide.

Why Pure Renewables Are Not Enough, Yet

There is a lot of pressure to frame every energy conversation around 100% renewable power. For data centers, that framing misses the operational reality.

Solar and wind are essential, but on their own, they do not solve the uptime problem. Delivering continuous power from pure renewables would require massive deployment of storage, deep grid flexibility, and substantial redundancy. In most markets, that is still expensive, complex, or simply not available at the scale hyperscalers need.

So the practical model, at least for now, is different.

The near-term winners will not be the companies promising pure green electrons. They will be the ones offering credible, bankable, always-available clean-ish power bundles, blending renewables with gas, nuclear, storage, and grid services.

That may not be the simplest message. But it is the one the market is likely to reward.

The New Strategic Buyers: Hyperscalers and AI Platforms

The rise of hyperscalers is reshaping the power market in real time.

Global technology players like Microsoft, AWS, G42, and xAI are not just buying rack space. They are influencing where infrastructure gets built, how power contracts are structured, and which energy partners gain long-term strategic value.

This changes the role of energy companies.

Instead of only selling electricity into the grid, they now have an opening to co-develop integrated infrastructure platforms that combine:

Power generation.

Grid access.

Backup reliability.

Renewable supply.

Cooling and water planning.

Long-term power purchase agreements.

AI-driven energy optimization.

That is a much higher-value position than being a commodity supplier.

Where the Biggest Value Will Be Captured

The most attractive opportunity is not simply generating more electricity. It is solving the full-power problem for large-scale digital infrastructure.

Energy companies that move early can create a defensible advantage in three areas.

1. AI-optimized operations

AI is in increasing demand, but it can also improve the supply side. Operators that use AI for load forecasting, dispatch optimization, predictive maintenance, and efficiency gains can improve reliability while lowering operating costs.

2. Long-term PPAs

Secure, long-duration PPAs will become central to the economics of new data center projects. The companies that can structure attractive, flexible contracts with credible low-carbon elements will stand out.

3. Co-development with hyperscalers

The strongest position will go to players who help design infrastructure from day one, rather than stepping in later as power vendors. Co-development creates deeper partnerships, stronger revenue visibility, and a better chance to influence siting and scaling decisions.

Why This Matters Beyond Energy

This shift will influence more than utilities and oil majors.

It will affect industrial policy, real estate development, digital infrastructure investors, technology platforms, and governments trying to turn national AI ambitions into real economic output.

In practical terms, every new hyperscale or AI-ready data center creates follow-on demand across:

Power infrastructure.

Water and cooling systems.

Transmission upgrades.

Land development.

Construction.

Equipment supply chains.

Cybersecurity and resilience services.

So while the headline story is about electricity, the broader story is about control over the infrastructure layer of the digital economy.

The New MENA Energy Model

The old model was straightforward: produce hydrocarbons, export energy, build around resource strength.

The new model is more strategic. Generate diversified power, anchor domestic digital infrastructure, attract AI investment, and turn energy advantage into compute advantage.

That is the real shift underway.

MENA is not simply trying to decarbonize. It is trying to become the place where low-cost energy, digital ambition, and infrastructure scale come together.

And that creates a rare opening for regional energy leaders.

The companies that win will not be the ones selling the cheapest electrons or the greenest story. They will be the ones that can offer reliability, carbon improvement, contract certainty, and strategic partnership in one package.

That is what the next wave of demand will pay for.

date published

May 15, 2026

reading time

8 min read